Brady Sidwell

Sidwell Strategies

Sat Jul 26, 8:24AM CDT

Howdy market watchers!

Only a few days remaining in July and it rained! Just as the delayed summer heat was beginning to turn conditions dryer, storms rolled in across the Southern Plains after covering the Midwest last weekend. Late July rains are a novelty and very welcome for agriculture. Pasture conditions have significantly improved with hay volume and quality as well as grass forage plentiful.

While the drought monitor continues to improve from the central US all the way to the eastern seaboard, western parts of the country are suffering from increasingly significant drought conditions.

US corn conditions remain elevated at 74 percent Good-to-Excellent (G/E), which is the best in nine years for mid-July. Soybean conditions came in at 68 percent G/E this week, three percent behind expectations, but still the best in 5 years for this time of year.

As winter wheat harvest progresses, now 73 percent complete in the US, spring wheat conditions came in 3 percentage points below expectations at 52 percent G/E this week versus 77 percent last year. This could support the overall wheat complex in the near-term.

The Wheat Quality Council’s spring wheat crop tour this week concluded with a forecast yield of 49.0 bushels per acre (bpa) for North Dakota, an entire 10.0 bpa below USDA’s current estimate of 59.0 bpa, matching last year’s record yield for the state despite conditions being 25 percent below last year’s G/E rating at this time of the year. I would expect a revision in USDA’s next monthly report in mid-August.

Europe wheat harvest is well underway with the largest producer, France, now 86 percent complete, ahead of last year when heavy rains at harvest delayed harvest and compromised quality. Ukraine’s wheat harvest has only collected half of the volume harvested at this time last year. We’ve heard mixed reports of wheat conditions in the Black Sea region including Russia with some areas much lower than expected due to drought while other areas are seeing increased yields. We’ve seen Russian wheat export prices declining recently after some rain delays supported prices just recently. However, US SRW is now the cheapest wheat in the world, which we’ve seen from strong US exports of wheat this week.

Despite this supportive news, it has been a choppy week for the wheat complex. Tuesday’s outside reversal higher chart day failed to get follow-through to the upside as such technical move suggests. Friday’s low in Chicago wheat futures was a new low for the week, but held above the prior low on July 17th. KC futures held above the week’s low on Friday after making a high above Thursday’s high and closing above the 9-day moving average and right below the 20-day moving average. Friday’s close on MATIF European wheat futures was disappointing near the week’s low, but did not make a new low.

Signs of stronger demand are needed to balance larger crops. The same goes for row crop forecasts with no major concerns to the large and growing crop. Having said that, these price levels are already pricing in a large crop, but with every passing week, we are getting closer to ‘made’ crops with concerns fading for any major changes to greatly impact trendline yields.

Next week’s August 1st deal deadline or risk higher tariffs from the US has the potential to bring volatility back to the markets, including for grains. Deals announced with Vietnam, Indonesia, Bangladesh, Japan and possibly the EU could add greater demand for US exports. The Trump Administration announced late this week about the Australian market opening to US beef while Bangladesh is committing to US wheat purchases that largely purchase from Russia, Ukraine and Canada.

Such news is more than welcome as China continues to shy away from purchasing US grains. Hopes returned for a minute this Thursday when the USDA accidently announced that China purchased US corn, but later said it was incorrect. The Trump Administration continues to work on a trade deal with China that could bring about such headlines, but it is a precarious situation and hard to count on anytime soon.

The ongoing conflict between Russia and the Ukraine is also relevant in the context of China as Putin continues to ramp up attacks despite Trump’s effort to facilitate negotiations. Russia and the Ukraine were to meet in Turkey this week, but nothing came of it has expected. Meanwhile, Trump has started to send weapons again to the Ukraine to defend against relentless drone attacks from Russia. There is now a deadline for Russia to come to the table or escalated sanctions to be placed on them including secondary tariffs on their trade partners, chief among them being China.

The US dollar bounced off lows to end the week, but remains under pressure. The FOMC meets this next week to vote on interest rates that will be announced on Wednesday, July 30th. While there is mounting pressure from President Trump on Chair Powell to cut interest rates, the data hardly suggests it is time. There is also a committee of 12 Governors and Regional Bank Presidents that have a vote. The odds of a rate cut at the September meeting are higher than the potential at next week’s meeting with another pause largely expected.

And yet, the stock market and cattle market continue to trade to new highs! The Dow Jones made a new high on Wednesday while the S&P 500 closed Friday at a new high.

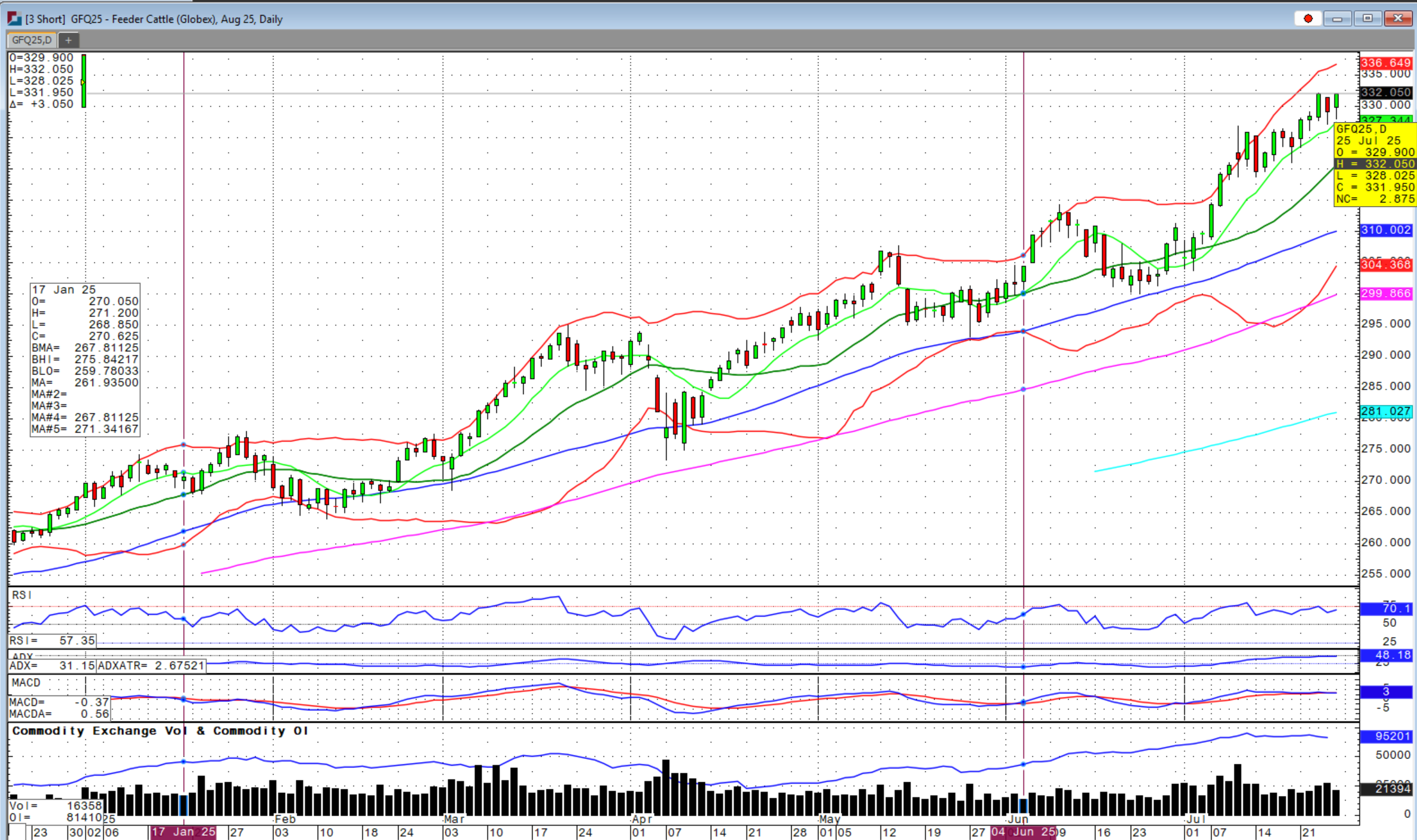

As go the equity markets, so go cattle. After choppy intra-day ranges, feeder cattle futures beyond August made new highs Friday. Live cattle futures made new highs on Wednesday, but did not trade above those levels on Friday despite a positive close. Cash fed cattle emerged strong this week reaching $232 in Texas and Kansas and $245 in Nebraska! The numbers just keep getting bigger.

Friday afternoon brought some fresh news to the market after the close. USDA’s monthly Cattle-on-Feed showed on-feed numbers as of July 1st were lower than expected at 98.4 percent of last year versus 99.2 percent forecast. This was an 8-year low. June placements were sharply lower than expected at 92.1 percent of last year versus 98.0 percent expected, which was a 16-year low. June marketings were lower than expected at 95.6 percent of last year versus 96.4 percent anticipated. Overall, these figures present a bullish bias to the cattle complex with lower on-feed and much lower placements versus expectations.

USDA’s bi-annual cattle inventory report was also released on Friday with total cattle and calf inventory as of July 1, 2025, at 94.2 million head compared to 95.40 million head on July 1, 2023, given there was no July 2024 report. This is a 70 year low for all cattle/calf inventory and came to 98.7 percent of the 2023 number versus 98.1 percent expected. For just beef cows, numbers came in at 98.8 percent versus 97.8 percent expected. Dairy cows came in at 100.5 percent and so slightly above 2023 levels. Annual calf crop numbers came in at 98.6 percent versus 97.8 percent expected.

While some of these inventory numbers were higher than expected, the headline of a 70-year low and bullish Cattle-on-Feed report suggest that this new news should continue to feed the bulls in the cattle complex. There is talk that August feeders could get as high as $353! What and when will the ‘Black Swan’ be in this market is an answer getting more valuable by the trading day, but for now it seems that nothing can shake the upward trajectory. For meat packers, the more the kill, the more they lose and yet, it continues.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available.

It is never too late to start and there is no operation too small to get a risk management and marketing plan in place. Wishing everyone a successful trading week!

Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

This article contains syndicated content. We have not reviewed, approved, or endorsed the content, and may receive compensation for placement of the content on this site. For more information please view the Barchart Disclosure Policy here.